29 Aug Compound Returns: Eighth Wonder of the World?

If you’re like most people, you need your investments to grow to achieve the life you want. Fortunately, there’s a deceptively simple but exceptionally powerful tool that can help you produce that growth. It’s called compounding, and it’s the process of earning investment returns on your past investment returns. Compound returns are such a big deal that they have been called the eighth wonder of the world (an expression likely misattributed to Albert Einstein).

The Wonders of Compounding

What puts compounding on par with the Great Pyramid at Giza? It can help your portfolio grow exponentially over time. Take this simplified (very) hypothetical example:

- You invest $10,000 and earn a 10% return the first year. In this example, your returns compound annually, so by the end of the year you have an additional $1,000.

- Now you have a total of $11,000. You keep it invested and earn another 10% return the next year.

- Since you started with more money, your 10% return produces a larger gain in dollar terms than it did the first year: $1,100 rather than $1,000.

The more your investments grow, the more you get to reinvest in pursuit of more growth.

You can pull a couple key levers to make the most of compounding. Using them wisely could give your savings a considerable boost. Let’s take a look:

Give It Time

In investing, time makes it possible for wealth to snowball. The longer you can allow your investment returns to compound, the greater the snowballing effect can be.

Thanks to compounding, money you invest early can become much more valuable than money you invest later in life. Many investors already get this on an intuitive level. But it can help to look at real (simple) numbers:

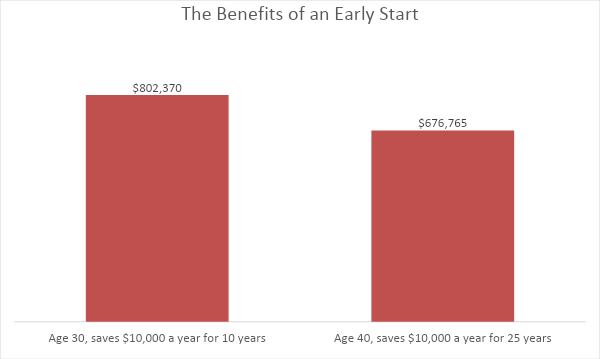

Jane, age 30, invests $10,000 dollars a year for 10 years and earns a 7% annual return. At the end of the decade, she has contributed $100,000. At that point she stops making contributions and leaves her money to keep earning 7% annually.

Total portfolio value at age 65: $802,370

Justin, age 40, is trying to catch up. He invests $10,000 a year for 25 years, and also earns a 7% annual return. His total contributions add up to $250,000. His portfolio’s value at age 65 is about $125,000 less than Jane’s, even though he contributed $150,000 more!

Total portfolio value at age 65: $676,765

[This hypothetical example shows how the earlier a person takes advantage of compound interest, the more time that money has to grow. Assumes a 7 interest rate, compounded annually. SOURCE: Author’s calculations.]

Bottom Line: The earlier you can start investing and taking advantage of compounding, the better. Even if you can only invest $25/month, it’s worth starting that snowball!

Make the Most of Tax Advantages

Taxes drain compounding’s strength. If you hold investments in a taxable account, their interest payouts, dividends, and realized capital gains can trigger taxes that effectively reduce your annual return. Lower effective returns leave less money to grow the next year.

It’s a different story if you hold your portfolio in a tax-advantaged account such as a 401(k), traditional IRA, or Roth IRA. You don’t pay taxes on money while it’s in these accounts, so every dollar of gains can go to work for you.

Now, that’s not to say you won’t pay taxes eventually. You contribute pre-tax money to traditional 401(k)s and IRAs, and it can grow tax-deferred while in the accounts. When you withdraw money after age 59 ½, the money you take out will be taxed at ordinary income tax rates. In the meantime, however, tax-advantaged compounding can help you build a considerably larger nest egg.

Roth accounts, on the other hand, are funded with after-tax dollars. Money inside the accounts grows tax-free, and you don’t pay taxes on withdrawals made after age 59 ½. In essence, any compound investment growth in a Roth is tax-free. Roths have income limits; ensure you qualify before starting.

Bottom Line: Investing inside tax-advantaged accounts can help your portfolio grow even faster by preserving more of any growth for longer.

Control What You Can

Like most things in life, investing includes many elements you can’t control, so it’s essential to focus on what you can—especially those moves that help you make the most of compounding. That’s why starting early, staying invested for the long term, and capitalizing on tax-advantaged accounts are critical for investing toward your long-term goals.

Please share this article with a young person you know – it’s never too early to start! Let us know if you have any questions about this or any other financial puzzle.

Information is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products, or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this post (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of Angela Wright, an Investment Adviser Representative of Gemmer Asset Management LLC (“GAM”) and should not be regarded as the views of GAM, or a description of advisory services provided by GAM or performance returns of any GAM client. References to securities or market-related performance data are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.